Context

This project is the end of term assignment in the Discriminant Analysis course led by Prof. Salim Lardjane, UBS.

Goals

The project has 2 main goals:

- be familiar with standard machine learning models

- implement from scratch those algorithms to understand the underlying statistics

Loading in the libraries

We’ll be reading a file containing information regarding the financial situation of a person to know weather this person is fit to pay the default or not.

1

2

3

4

5

6

7

8

9

10

library(foreign)

library(MASS)

library(ROCR)

library(mlogit)

library(caTools)

library(e1071)

library(ggplot2)

library(ROCit)

library("tidyverse")

data <- read.spss("./bankloan.sav",to.data.frame=TRUE)

Descriptive analysis

1

summary(data)

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

## age ed employ

## Min. :20.00 Did not complete high school:460 Min. : 0.000

## 1st Qu.:29.00 High school degree :235 1st Qu.: 3.000

## Median :34.00 Some college :101 Median : 7.000

## Mean :35.03 College degree : 49 Mean : 8.566

## 3rd Qu.:41.00 Post-undergraduate degree : 5 3rd Qu.:13.000

## Max. :56.00 Max. :33.000

## address income debtinc creddebt

## Min. : 0.000 Min. : 13.00 Min. : 0.10 Min. : 0.0117

## 1st Qu.: 3.000 1st Qu.: 24.00 1st Qu.: 5.10 1st Qu.: 0.3822

## Median : 7.000 Median : 35.00 Median : 8.70 Median : 0.8851

## Mean : 8.372 Mean : 46.68 Mean :10.17 Mean : 1.5768

## 3rd Qu.:12.000 3rd Qu.: 55.75 3rd Qu.:13.80 3rd Qu.: 1.8984

## Max. :34.000 Max. :446.00 Max. :41.30 Max. :20.5613

## othdebt default preddef1 preddef2

## Min. : 0.04558 No :517 Min. :0.0001166 Min. :0.0000387

## 1st Qu.: 1.04594 Yes :183 1st Qu.:0.0456301 1st Qu.:0.0351757

## Median : 2.00324 NA's:150 Median :0.1715129 Median :0.1590730

## Mean : 3.07879 Mean :0.2585762 Mean :0.2578660

## 3rd Qu.: 3.90300 3rd Qu.:0.4073259 3rd Qu.:0.4332770

## Max. :35.19750 Max. :0.9993967 Max. :0.9994570

## preddef3

## Min. :0.07464

## 1st Qu.:0.13476

## Median :0.20010

## Mean :0.25858

## 3rd Qu.:0.32863

## Max. :0.94810

Discriminant Analysis without cross-validation

Separating the data (train/test)

1

2

3

4

5

6

7

8

9

10

11

12

13

14

library(MASS)

library(e1071)

na <- c(701:850)

apred <- data[na,] # the data that we're going to predict later on, once our models are trained

data2 <- subset(data, data$default != "NA'S") # the data we'll use for the train/test datasets

data2<-data2[1:9]

data2<-data2[-2]

data2[,8]<-as.numeric(data2$default)-1

n = dim(data2)[1]

id = sample(1:n,floor(0.75*n),replace=F)

train <- data2[id,]

test <- data2[-id,]

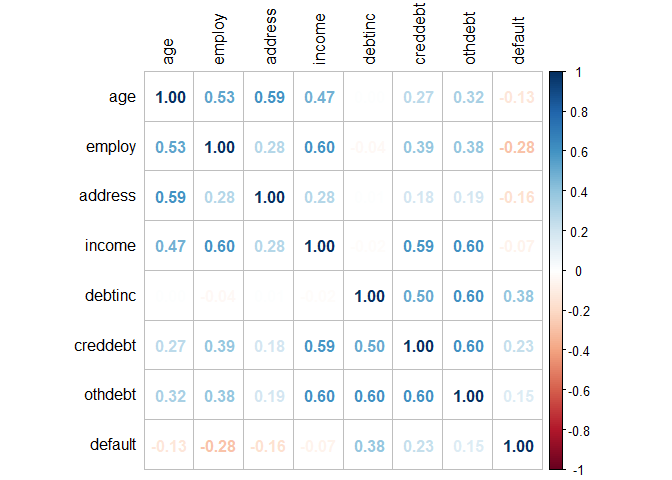

Correlation coefficient visualization

1

2

3

4

5

6

7

8

9

library(corrplot)

corrplot(cor(train), # Correlation matrix

method = "number", # Correlation plot method

type = "full", # Correlation plot style (also "upper" and "lower")

diag = TRUE, # If TRUE (default), adds the diagonal

tl.col = "black", # Labels color

bg = "white", # Background color

title = "", # Main title

col = NULL) # Color palette

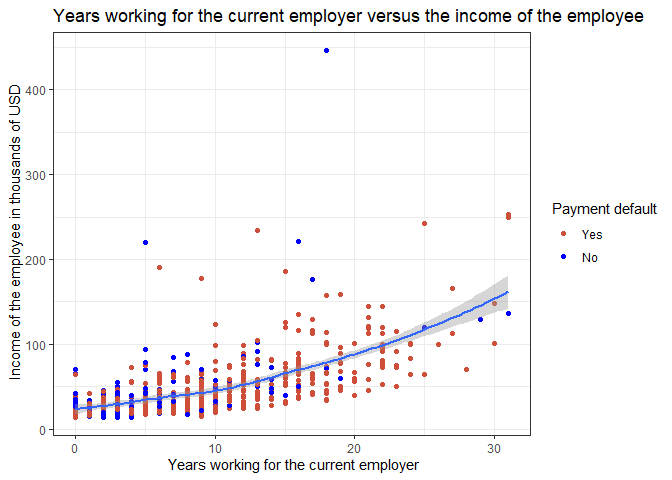

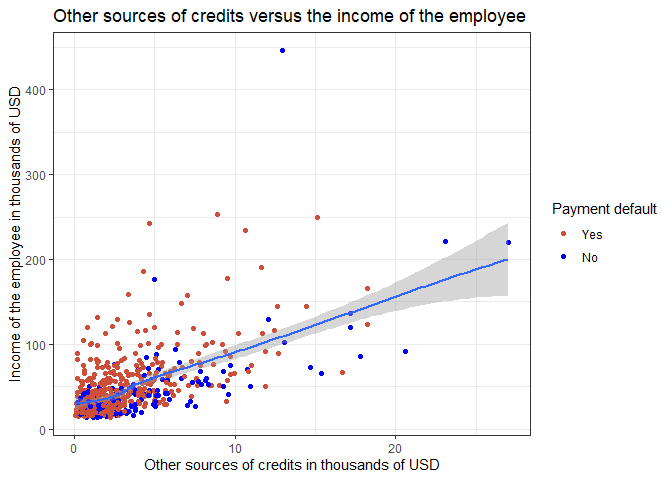

Graphs

In order to find the best way to represent our data, we’ll sort the variables in 3 classes : stability, demographic and financial data.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

# stability variables : employ address

# demographic variables : age

# financial variables : income debtinc creddebt othdebt

# employ income

data2 %>% mutate(default = factor(default)) %>%

ggplot(aes(x = employ, y = income)) +

geom_point(mapping = aes(color = default)) +

labs(x=" Years working for the current employer",

y=" Income of the employee in thousands of USD",

color = "Payment default") +

geom_smooth() +

scale_color_manual(values = c("0" = "tomato3",

"1" = "blue"),

labels = c("Yes",

"No")) +

theme_bw()+

ggtitle("Years working for the current employer versus the income of the employee")

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

# othdebt income

data2 %>% mutate(default = factor(default)) %>%

ggplot(aes(x = othdebt, y = income)) +

geom_point(mapping = aes(color = default)) +

labs(y="Income of the employee in thousands of USD",

x="Other sources of credits in thousands of USD",

color = "Payment default") +

geom_smooth() +

scale_color_manual(values = c("0" = "tomato3",

"1" = "blue"),

labels = c("Yes",

"No")) +

theme_bw()+

ggtitle("Other sources of credits versus the income of the employee")

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

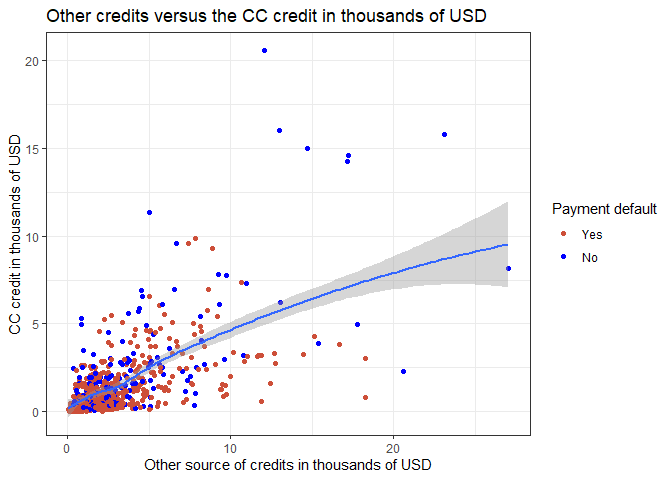

# othdebt creddebt

data2 %>% mutate(default = factor(default)) %>%

ggplot(aes(x = othdebt, y = creddebt)) +

geom_point(mapping = aes(color = default)) +

labs(y="CC credit in thousands of USD",

x="Other source of credits in thousands of USD",

color = "Payment default") +

geom_smooth() +

scale_color_manual(values = c("0" = "tomato3",

"1" = "blue"),

labels = c("Yes",

"No")) +

theme_bw()+

ggtitle("Other credits versus the CC credit in thousands of USD")

Defining the ROC function

This function will allow us to trace a ROC curve for each model that returns posterior probabilities

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

roc <- function(post1, col){

trapeze <- function(ao,bo) {

k <- length(ao)

iz <- 0

for (i in 1:(k-1)) {

iz <- iz+(ao[i+1]-ao[i])*(bo[i]+bo[i+1])/2

}

return(iz)

}

delta=0.001

valeurs <- seq(0,1,delta)

N <- length(valeurs)

sensibilite <- rep(NA,N)

antispec <- rep(NA,N)

i <- 0

for (u in valeurs) {

i <- i+1

pr2predict <- (post1>u)+0

TN1 <- sum((pr2predict==0)*(test$default==0))

FP1 <- sum((pr2predict==1)*(test$default==0))

FN1 <- sum((pr2predict==0)*(test$default==1))

TP1 <- sum((pr2predict==1)*(test$default==1))

Rap1 <- TP1/(TP1+FN1)

Pre1 <- TP1/(TP1+FP1)

F_sco1 <- (2*TP1)/(2*TP1+FP1+FN1)

Spe1 <- TN1/(FP1+TN1)

Err1 <- ((FP1+FN1)/(TN1+FP1+TP1+FN1)*100)

sensibilite[i] <- Rap1

antispec[i] <- 1-Spe1

}

antispec<- c(0,rev(antispec),1)

sensibilite <- c(0,rev(sensibilite),1)

plot(antispec,sensibilite,type="s",col=col,lwd=1)

return(trapeze(antispec, sensibilite))

}

Defining the models

For each model we’ll compute recall, f-score, acc, specificity and add the values to a dataframe that we’ll comment at the end.

Closest Mean method

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

no.age <- mean(train[train$default==0,]$age)

yes.age <- mean(train[train$default==1,]$age)

no.employ <- mean(train[train$default==0,]$employ)

yes.employ <- mean(train[train$default==1,]$employ)

no.address <- mean(train[train$default==0,]$address)

yes.address <- mean(train[train$default==1,]$address)

no.income <- mean(train[train$default==0,]$income)

yes.income <- mean(train[train$default==1,]$income)

no.debtinc <- mean(train[train$default==0,]$debtinc)

yes.debtinc <- mean(train[train$default==1,]$debtinc)

no.creddebt <- mean(train[train$default==0,]$creddebt)

yes.creddebt <- mean(train[train$default==1,]$creddebt)

no.othdebt <- mean(train[train$default==0,]$othdebt)

yes.othdebt <- mean(train[train$default==1,]$othdebt)

prediction <- function(x,y,z,a,b,c,d) {

if ((x-yes.age)^2+(y-yes.employ)^2+(z-yes.address)^2+(a-yes.income)^2+(b-yes.debtinc)^2+(c-yes.creddebt)^2+(d-yes.othdebt)^2 >(x-no.age)^2+(y-no.employ)^2+(z-no.address)^2+(a-no.income)^2+(b-no.debtinc)^2+(c-no.creddebt)^2+(d-no.othdebt)^2)

{

return(1)

} else {return(0)}

}

pred <- rep(NA,length(test$default))

for (i in 1:length(test$default)) {

pred[i] <- prediction(test$age[i],test$employ[i],test$address[i], test$income[i], test$debtinc[i], test$creddebt[i], test$othdebt[i])

}

MCPPM = table(pred,test$default)

MCPPMerr = (MCPPM[2,1]+MCPPM[1,2])/sum(MCPPM)

MCPPMrappel = MCPPM[2,2]/(MCPPM[2,2]+MCPPM[1,2])

MCPPMprecision = MCPPM[2,2]/(MCPPM[2,2]+MCPPM[2,1])

MCPPMF = 2*MCPPM[2,2]/(2*MCPPM[2,2]+MCPPM[2,1]+2*MCPPM[1,2])

MCPPMspecificite = MCPPM[2,2]/(MCPPM[2,2]+MCPPM[2,1])

PPM = round(c(MCPPMerr,MCPPMrappel,MCPPMprecision,MCPPMF,MCPPMspecificite),2)

Quadratic Discriminant Analysis method

1

2

3

4

5

6

7

8

9

10

11

library(MASS)

model = predict(qda(default~.,train),test)

MCqda = table(test$default,model$class) # correlation matrix

MCqdaerr = (MCqda[2,1]+MCqda[1,2])/sum(MCqda)

MCqdarappel = MCqda[2,2]/(MCqda[2,2]+MCqda[1,2])

MCqdaprecision = MCqda[2,2]/(MCqda[2,2]+MCqda[2,1])

MCqdaF = 2*MCqda[2,2]/(2*MCqda[2,2]+MCqda[2,1]+2*MCqda[1,2])

MCqdaspecificite = MCqda[2,2]/(MCqda[2,2]+MCqda[2,1])

qda = round(c(MCqdaerr,MCqdarappel,MCqdaprecision,MCqdaF,MCqdaspecificite),2)

Linear Discriminant Analysis method

1

2

3

4

5

6

7

8

9

10

11

library(MASS)

model = predict(lda(default~.,train),test)

MClda = table(test$default,model$class)

MCldaerr = (MClda[2,1]+MClda[1,2])/sum(MClda)

MCldarappel = MClda[2,2]/(MClda[2,2]+MClda[1,2])

MCldaprecision = MClda[2,2]/(MClda[2,2]+MClda[2,1])

MCldaF = 2*MClda[2,2]/(2*MClda[2,2]+MClda[2,1]+2*MClda[1,2])

MCldaspecificite = MClda[2,2]/(MClda[2,2]+MClda[2,1])

lda = round(c(MCldaerr,MCldarappel,MCldaprecision,MCldaF,MCldaspecificite),2)

Naive Bayes method

1

2

3

4

5

6

7

8

9

10

11

library(e1071)

model = predict(naiveBayes(default~.,train),test)

MCbayes = table(test$default,model)

MCbayeserr = (MCbayes[2,1]+MCbayes[1,2])/sum(MCbayes)

MCbayesrappel = MCbayes[2,2]/(MCbayes[2,2]+MCbayes[1,2])

MCbayesprecision = MCbayes[2,2]/(MCbayes[2,2]+MCbayes[2,1])

MCbayesF = 2*MCbayes[2,2]/(2*MCbayes[2,2]+MCbayes[2,1]+2*MCbayes[1,2])

MCbayesspecificite = MCbayes[2,2]/(MCbayes[2,2]+MCbayes[2,1])

bayes = round(c(MCbayeserr,MCbayesrappel,MCbayesprecision,MCbayesF,MCbayesspecificite),2)

K closest neighbours method

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

library(class)

cl <- as.factor(train$default)

predtest <- knn(train,test,cl, k=1)

MCknn1 = table(test$default,predtest)

MCknn1err = (MCknn1[2,1]+MCknn1[1,2])/sum(MCknn1)

MCknn1rappel = MCknn1[2,2]/(MCknn1[2,2]+MCknn1[1,2])

MCknn1precision = MCknn1[2,2]/(MCknn1[2,2]+MCknn1[2,1])

MCknn1F = 2*MCknn1[2,2]/(2*MCknn1[2,2]+MCknn1[2,1]+2*MCknn1[1,2])

MCknn1specificite = MCknn1[2,2]/(MCknn1[2,2]+MCknn1[2,1])

knn1 = round(c(MCknn1err,MCknn1rappel,MCknn1precision,MCknn1F,MCknn1specificite),2)

predtest <- knn(train,test,cl, k=2)

MCknn2 = table(test$default,predtest)

MCknn2err = (MCknn2[2,1]+MCknn2[1,2])/sum(MCknn2)

MCknn2rappel = MCknn2[2,2]/(MCknn2[2,2]+MCknn2[1,2])

MCknn2precision = MCknn2[2,2]/(MCknn2[2,2]+MCknn2[2,1])

MCknn2F = 2*MCknn2[2,2]/(2*MCknn2[2,2]+MCknn2[2,1]+2*MCknn2[1,2])

MCknn2specificite = MCknn2[2,2]/(MCknn2[2,2]+MCknn2[2,1])

knn2 = round(c(MCknn2err,MCknn2rappel,MCknn2precision,MCknn2F,MCknn2specificite),2)

predtest <- knn(train,test,cl,k=3)

MCknn3 = table(test$default,predtest)

MCknn3err = (MCknn3[2,1]+MCknn3[1,2])/sum(MCknn3)

MCknn3rappel = MCknn3[2,2]/(MCknn3[2,2]+MCknn3[1,2])

MCknn3precision = MCknn3[2,2]/(MCknn3[2,2]+MCknn3[2,1])

MCknn3F = 2*MCknn3[2,2]/(2*MCknn3[2,2]+MCknn3[2,1]+2*MCknn3[1,2])

MCknn3specificite = MCknn3[2,2]/(MCknn3[2,2]+MCknn3[2,1])

knn3 = round(c(MCknn3err,MCknn3rappel,MCknn3precision,MCknn3F,MCknn3specificite),2)

Logistic regression model

Preparing the data

1

data2$default <- as.factor(data2$default)

Defining the model

1

2

3

4

5

6

reglog <- glm(default~., family = binomial, data=train, control=list(maxit=1000, trace=TRUE, epsilon=1e-16))

preds <- predict(reglog, test, type='response')

optimal_cutoff <- ifelse(preds > 0.5, 1, 0)

summary(reglog)

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

##

## Call:

## glm(formula = default ~ ., family = binomial, data = train, control = list(maxit = 1000,

## trace = TRUE, epsilon = 1e-16))

##

## Deviance Residuals:

## Min 1Q Median 3Q Max

## -2.3241 -0.6734 -0.3020 0.2628 2.6057

##

## Coefficients:

## Estimate Std. Error z value Pr(>|z|)

## (Intercept) -1.657904 0.664307 -2.496 0.0126 *

## age 0.044607 0.020375 2.189 0.0286 *

## employ -0.268156 0.037089 -7.230 4.82e-13 ***

## address -0.113424 0.027131 -4.181 2.91e-05 ***

## income -0.008652 0.008473 -1.021 0.3072

## debtinc 0.067861 0.035900 1.890 0.0587 .

## creddebt 0.611694 0.134228 4.557 5.19e-06 ***

## othdebt 0.080870 0.085357 0.947 0.3434

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## (Dispersion parameter for binomial family taken to be 1)

##

## Null deviance: 602.75 on 524 degrees of freedom

## Residual deviance: 418.16 on 517 degrees of freedom

## AIC: 434.16

##

## Number of Fisher Scoring iterations: 7

1

2

3

4

5

6

7

8

9

#confusion matrix

MCreg = table(test$default, optimal_cutoff)

MCregerr = (MCreg[2,1]+MCreg[1,2])/sum(MCreg)

MCregrappel = MCreg[2,2]/(MCreg[2,2]+MCreg[1,2])

MCregprecision = MCreg[2,2]/(MCreg[2,2]+MCreg[2,1])

MCregF = 2*MCreg[2,2]/(2*MCreg[2,2]+MCreg[2,1]+2*MCreg[1,2])

MCregspecificite = MCreg[2,2]/(MCreg[2,2]+MCreg[2,1])

reg = round(c(MCregerr,MCregrappel,MCregprecision,MCregF,MCregspecificite),2)

1

2

titles = c("Error rate","Recall","Accuracy","F-Score","Specificity")

data.frame(titles,lda,qda,knn1,knn2,knn3,PPM, reg)

1

2

3

4

5

6

## titles lda qda knn1 knn2 knn3 PPM reg

## 1 Error rate 0.19 0.21 0.29 0.30 0.24 0.54 0.18

## 2 Recall 0.70 0.66 0.46 0.42 0.56 0.22 0.68

## 3 Accuracy 0.50 0.46 0.46 0.35 0.39 0.14 0.59

## 4 F-Score 0.52 0.47 0.36 0.30 0.39 0.13 0.55

## 5 Specificity 0.50 0.46 0.46 0.35 0.39 0.14 0.59

Disciminant Analysis with cross-validation method Leave-One-Out

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

55

56

57

58

59

60

61

62

63

64

65

66

67

68

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

100

101

102

103

104

105

106

107

108

109

data2$default <- as.numeric(data2$default)-1

n = dim(data2)[1]

lda = 0

qda = 0

naive = 0

knn1 = 0

knn2 = 0

knn3 = 0

ppm = 0

for(i in 1:n) {

train <- data2[-i,]

test <- data2[i,]

# LDA #

model = predict(lda(default~.,train),test)

erlda = (data2$default[i] != model$class) + 0

MClda = table(model$class,test$default)

lda[i] = erlda

# QDA #

model2 = predict(qda(default~.,train),test)

erqda = (data2$default[i] != model2$class) + 0

qda[i] = erqda

# Naive Bayes #

model3 = predict(naiveBayes(default~.,train),test)

ernaive = (data2$default[i] != model3) + 0

naive[i] = ernaive

# KNN #

cl <- as.factor(train$default)

# Prediction K=1 #

predtest <- knn(train,test,cl, k=1)

# errors K=1 #

erknn1 = (data2$default[i] != predtest) + 0

knn1[i] = erknn1

# Prediction K=2 #

predtest <- knn(train,test,cl, k=2)

# errors K=2 #

erknn2 = (data2$default[i] != predtest) + 0

knn2[i] = erknn2

# Prediction K=3 #

predtest <- knn(train,test,cl, k=3)

# errors K=3 #

erknn3 = (data2$default[i] != predtest) + 0

knn3[i] = erknn3

# Prediction for closest mean #

no.age <- mean(train[train$default==0,]$age)

yes.age <- mean(train[train$default==1,]$age)

no.employ <- mean(train[train$default==0,]$employ)

yes.employ <- mean(train[train$default==1,]$employ)

no.address <- mean(train[train$default==0,]$address)

yes.address <- mean(train[train$default==1,]$address)

no.income <- mean(train[train$default==0,]$income)

yes.income <- mean(train[train$default==1,]$income)

no.debtinc <- mean(train[train$default==0,]$debtinc)

yes.debtinc <- mean(train[train$default==1,]$debtinc)

no.creddebt <- mean(train[train$default==0,]$creddebt)

yes.creddebt <- mean(train[train$default==1,]$creddebt)

no.othdebt <- mean(train[train$default==0,]$othdebt)

yes.othdebt <- mean(train[train$default==1,]$othdebt)

prediction <- function(x,z,a,b,c,d,e) {

if ((x-yes.age)^2+(z-yes.employ)^2+(a-yes.address)^2+

(b-yes.income)^2+(c-yes.debtinc)^2+(d-yes.creddebt)^2+

(e-yes.othdebt)^2 >

(x-no.age)^2+(z-no.employ)^2+(a-no.address)^2+

(b-no.income)^2+(c-no.debtinc)^2+(d-no.creddebt)^2+

(e-no.othdebt)^2)

{

return(1)

} else {return(0)}

}

pred <- prediction(test$age,test$employ,test$address, test$income, test$debtinc, test$creddebt, test$othdebt)

erppm = (data2$default[i] != pred) + 0

ppm[i] <- erppm

}

validationCroisée = c("taux d'erreur")

res = c(mean(lda),mean(qda),mean(naive),mean(knn1),mean(knn2),mean(knn3), mean(ppm))

lda = mean(lda)

qda = mean(qda)

naive = mean(naive)

knn1 = mean(knn1)

knn2 = mean(knn2)

knn3 = mean(knn3)

ppm = mean(ppm)

data.frame(validationCroisée,lda,qda,naive,knn1,knn2,knn3,ppm)

1

2

3

4

## validationCroisée lda qda naive knn1 knn2 knn3

## 1 taux d'erreur 0.1871429 0.2228571 0.2471429 0.2842857 0.2928571 0.2471429

## ppm

## 1 0.5414286

Here we can see that the model with the smallest error rate is the LDA model.

Using our best model for the prediction on the data

1

2

model = predict(lda(default~.,data2),apred)

model$class

1

2

3

4

5

6

## [1] 0 0 1 0 0 0 0 1 0 0 0 0 0 0 0 1 1 0 1 0 0 0 0 0 0 0 0 0 0 0 0 0 1 0 0 0 0

## [38] 0 0 0 0 0 0 0 0 1 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 1 0 0 0 0 0 0 1 0 0 1

## [75] 0 0 0 0 0 0 0 1 0 1 1 0 0 0 0 1 0 0 0 0 0 0 0 0 0 1 0 1 0 1 0 0 0 1 0 0 1

## [112] 0 0 0 0 0 0 0 0 0 0 0 1 0 0 0 1 0 0 0 0 0 0 0 0 0 1 0 0 0 1 0 0 0 0 0 0 0

## [149] 0 0

## Levels: 0 1

1

2

3

4

5

6

7

8

9

10

yes = 0

no = 0

for (i in 1:150){

if(model$class[i] == 1){

yes=yes+1

}else{

no=no+1

}

}

yes

1

## [1] 23

1

no

1

## [1] 127

1

prediction = yes/150;prediction

1

## [1] 0.1533333

So out of 150 people, 23 are likely to repay their credit and 127 are not likely to repay their credit, iow -> 15.3% of the population